MAIN IDEA:

The main idea of this book is to review various potential causes of slowdown in GDP growth over the last 20 years and evaluate which of them has more and which has less impact. Author findings are that only demographics, shift from goods to services, and decline in population mobility have significant impact. Author also divides these causes into positive and negative, concluding that positive have more impact and therefore slowdown in growth is a sign of positive development.

DETAILS:

Preface

This starts with the point that until year 2000 average growth of USA economy was 2% per years, but after in decreased, but material standards of live actually continue to increase. Author then retells how this book started and who helped him to write it.

1. Victims of Our Own Success

In this chapter author starts by providing economic statistics: “The growth rate of GDP per capita, which is what I focus on in this book, averaged 2.25% per year from 1950 to 2000. But the average growth rate of GDP per capita from 2000 to 2016 was only 1%. That difference of 1.25 percentage points of growth per year means that GDP per capita today is about 25% lower than if we had matched the twentieth-century growth rate throughout the twenty-first century. It represents a significant deceleration of economic growth, but it started well before the recession in 2009.”

Then he discusses sources of growth, especially in human capital and demonstrates that its growth slowed. He also discusses switch from goods to services and how it slows growth because increase in productivity is much more difficult to achieve in services than in manufacturing. Finally, he briefly discusses different theories of slowdown. The final point in this chapter is that slowdown could be a good thing because it demonstrates that we achieved such high levels of productivity that the growth is not important anymore.

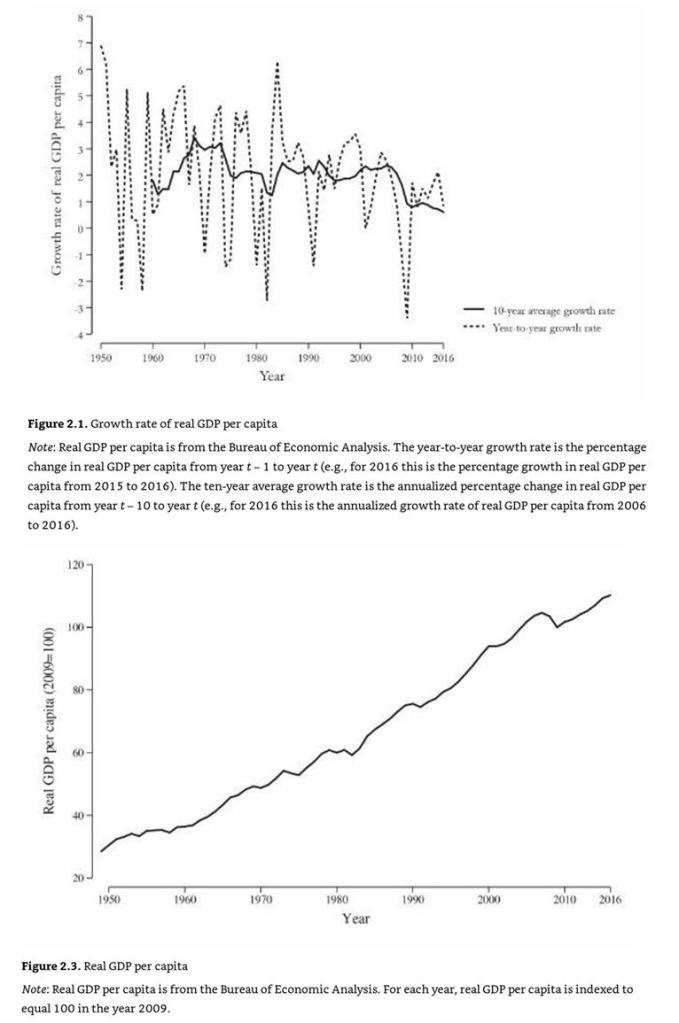

2. What Is the Growth Slowdown?

Here author starts with meaning and provides a nice illustration.

At the end of chapter author compares American data with other countries, demonstrating that it is not that different for developed European countries and Japan, but a lot less than China. Author also makes a point that growth slowdown does not mean that anything become worse than before, but rather that it does not getting better as fast as it could be.

3. The Inputs to Economic Growth

Here author discusses components of growth:

- Human capital as combination of number of employees, hours worked, and level of educations

- Physical capital as combination of structures, equipment, and intellectual property

He then explains that even if growth of all components decreased, it is not enough to explain decrease in aggregate

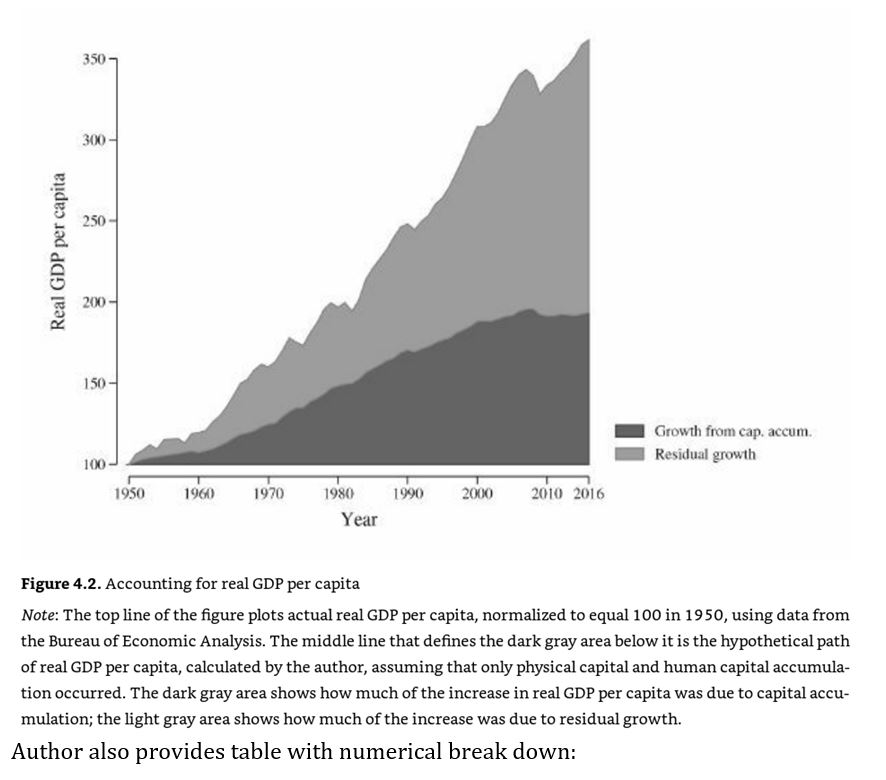

4 What Accounts for the Growth Slowdown?

Here author looks at data per capita and demonstrates that there is residual growth not explained by growth components and it is what slowed it down:

6. The Difference between Productivity and Technology

In this chapter author looks at technology and productivity and difference that could be related to both machines and processes. Author also discusses diminishing returns on R&D investment, asking if “we run out of innovations?”.

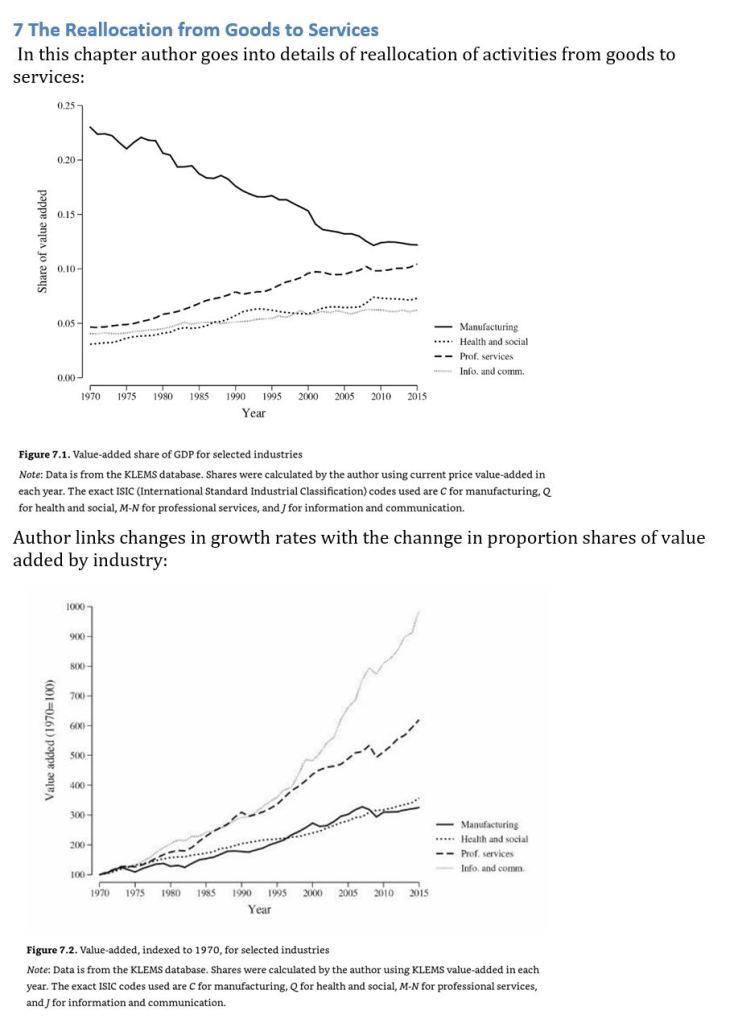

At the end of chapter author discusses potential explanations to residual:

- The first explanation involves the long-run shift in the composition of our spending away from goods and toward services.

- The second big idea for explaining slower productivity growth was the rise in market power of firms over the past few decades. The available evidence shows that the average markup—the ratio of price to marginal cost—charged by firms in the economy has increased since 1990. That rise in markups was consistent with the rise in economic profits as a share of GDP over the same time period.

- A last explanation for the slowdown in productivity growth is also a little puzzling. What I’ll document is that along a number of dimensions, the reallocation of human and physical capital between different uses has slowed down.

The final conclusion about market power is:” Increased market power was associated with a smaller share of GDP flowing toward labor or the providers of physical capital, and a larger share to the claimants on the economic profits market power creates. In general, that meant the owners of firms. There are reasons to be wary of that, even if, relative to changes in demographics and the long-run shift into services, it did not explain why the growth rate of real GDP per capita fell.”

12 Reallocations across Firms and Jobs; 13 The Drop in Geographic Mobility

Here author analyzes if reallocation is a source of slowdown in growth. He goes through reallocation within industries, slowing in turnover of establishments, job turnover, and geographic mobility, which also decreased. The conclusion is:” The decline in geographic mobility was not trivial, but it does not explain the growth slowdown.”

14 Did the Government Cause the Slowdown?

Here author reviews consequences of changes in taxes and other government policies and concludes: ”But the evidence indicates that taxation and regulation did not have a significant effect on the ability of firms to produce real goods and services, and specifically there was no substantial shift in government policies around 2000 that could explain the growth slowdown.”

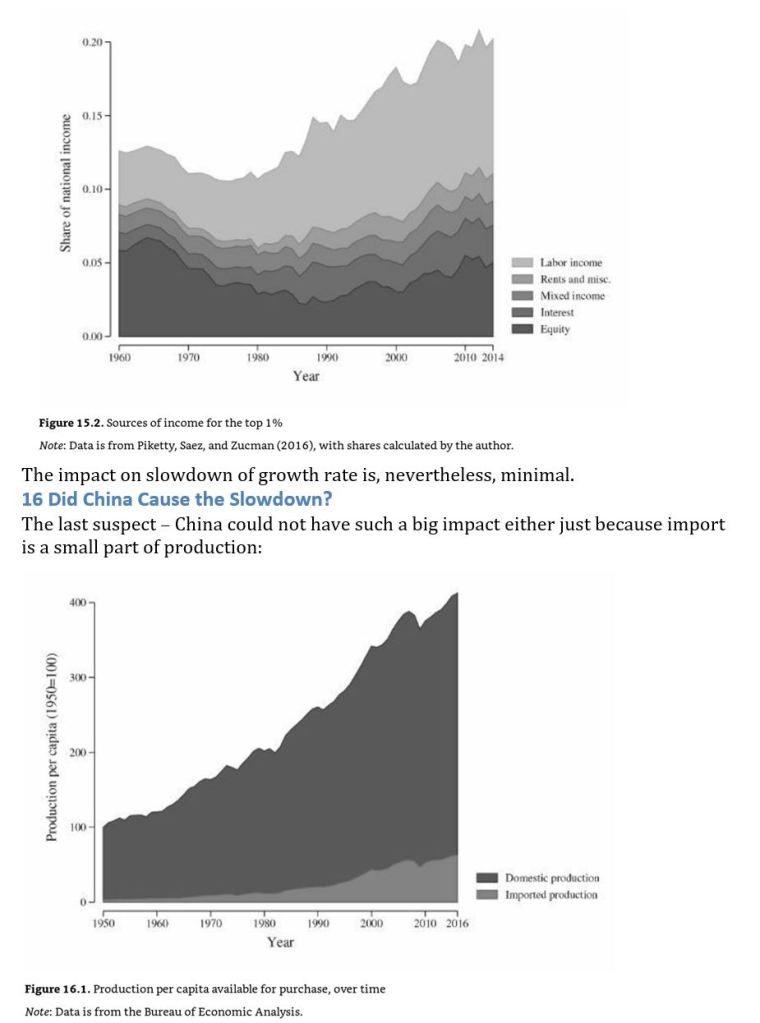

15 Did Inequality Cause the Slowdown?

Here author discusses changes in inequality and provides graph demonstrating that top 1% became less dependent on equity and more on labor income:

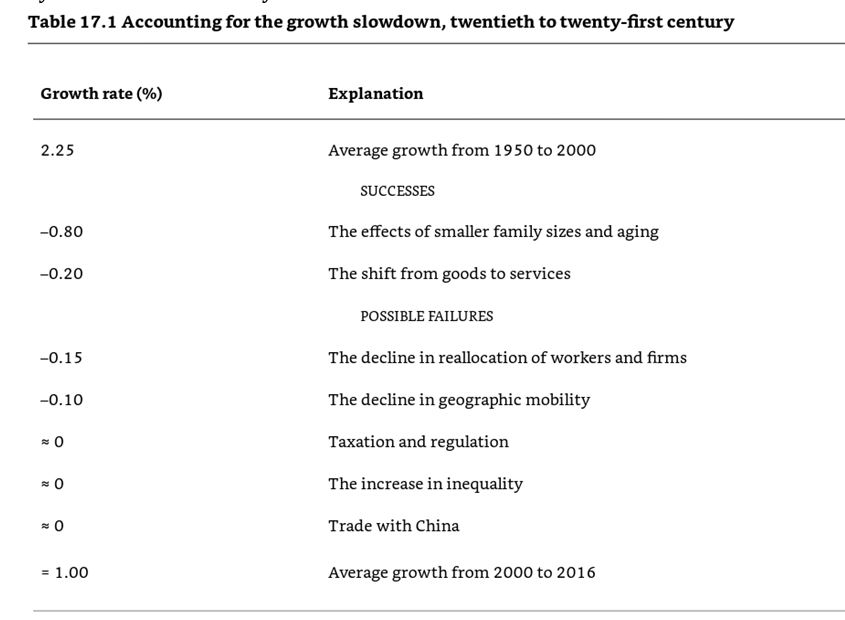

The conclusion: “Although the effect of Chinese trade was real in terms of replacing US manufacturing firms and employment—and that had real, negative impacts on those workers and their communities—in terms of the growth slowdown, the impact of Chinese trade was not large. The growth slowdown would have happened even if China had never become a major exporter, as the US was already in the middle of a long-run shift away from goods production toward services production. China accelerated this in a small way but was not responsible for it.”

17 The Future of Growth

In the final chapter author summarizes results of analysis concluding that causes of the growth slowdown are demographic and everything else has very small impact if any. Here is the summary:

At the end author looks in the future and expresses believe that even if the growth will not accelerate, it is actually sign of success because it is result of choices that people make and achieved wealth allows to make choices less bound by material needs than ever before.

MY TAKE ON IT:

From my point of view the accounting growth of GDP is pretty much meaningless number because it does not provide any direct information on material wellbeing of people and therefore requirement for such growth. For example. if everybody who wants to have steak dinner can do it any time, what is the point in growth of beef production? It applies to everything else: houses, cars, and so on. However, leaving aside the question who needs growth and why, the author’s conclusion that slowdown caused by mainly demographics in my view is technically correct, but missing the most important part – lots of people feel big gap between what is available to them materially and want they actually want to have and this gap is not result of inability to produce enough, but rather of ineffective organization of production and distribution processes. If this organization were modified so that its main objective become to close the gap, we would probably see initially huge growth, which then drop to near 0 when human aspirations switch away from material need to something else.